How the Invoice Factoring Process

Works Day to Day

A practical guide that shows what happens each funding cycle and what only happens occasionally.

Once your business is approved for invoice factoring, the process quickly becomes routine. After the initial setup, you don’t have to re-qualify. You simply follow the same steps each week.

Invoices are issued, submitted, and paid; funds are advanced; and balances are settled. When everything stays consistent, factoring runs quietly in the background as part of your cash flow operations.

This guide shows how invoice factoring works in daily business, making it clear which steps happen regularly and which are occasional.

- What happens every time you factor invoices, and

- What only happens occasionally or when something changes.

If you need more details about setup or how reserves work, you’ll find those topics in other articles:

- The complete invoice factoring approval and onboarding process

- A detailed explanation of how factoring reserves work

This article focuses on what happens once factoring is up and running.

Part 1: What Happens Every Day (or Every Funding Cycle)

These steps are part of the regular factoring process and repeat weekly, biweekly, or even daily, depending on how often you choose to sell your receivables.

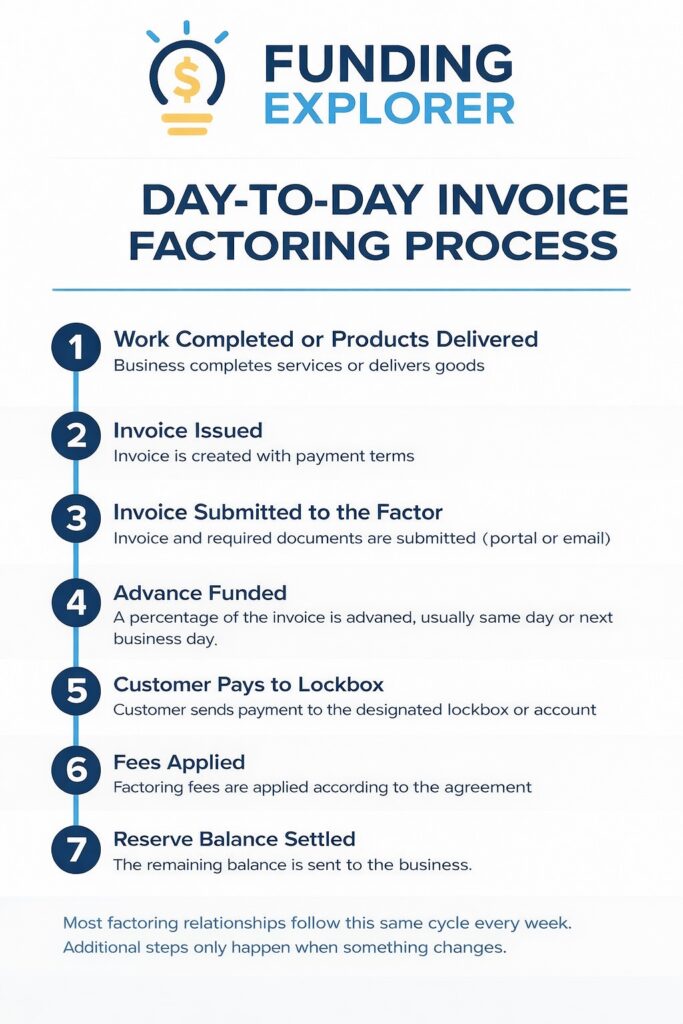

A Simple, Realistic Factoring Timeline

Here’s what a typical, smooth factoring cycle looks like:

- Work completed or products delivered

- Invoice issued

- Invoice submitted with documentation to the factor

- Advance funded

- Customer pays into the lockbox.

- Fees applied

- Reserve balance settled

Let’s look into the most important steps in this process.

Selling Your Invoices: How to Submit Invoices to a Factoring Company

Each funding cycle starts when you send your invoices to the factoring company. This process is not standard among factors. Each funder has its method for receiving requests.

Here are the most common invoice submission methods:

Online factoring portal

Many factoring companies use secure online systems where you can upload invoices and supporting documents. These systems also let you check your funding status, reserve balances, payment history, and invoice activity.

Portals often let you upload several invoices at once, making them a fast option for businesses with many invoices.

Email submissions

This method is still common. You email invoices and supporting documents to your account manager or the processing inbox. It works best when your files are complete and clearly labeled.

Hybrid setups

Some factoring companies let you send invoices by email, but you can track your funding status, reserve balances, and payment history online. You submit by email and monitor everything through their portal.

What Documents Factoring Companies Require With Each Invoice

Most factoring companies require the same basic documents each time you submit invoices:

- An invoice with a clear invoice number, date, amount, and payment terms

- Proof of work (delivery receipts, signed time sheets, bills of lading, work orders, or contracts)

- Purchase order, when applicable

- Sometimes, an assignment schedule for batch submissions

The main reason for funding delays is missing or inconsistent paperwork, not credit issues.

Assignment Schedules: When Factors Ask for Them

An assignment schedule is basically a list of factors that includes the invoices you’re selling, along with key details like customer names, invoice dates, and amounts.

Some factors want an assignment schedule with invoice submissions, and others don’t. Assignment schedules are more common when:

- Invoices are submitted in large batches.

- Posting is partially manual.

- Internal reconciliation controls require summaries.

And they are usually not required when:

- Invoices are uploaded individually through a portal.

- Automated posting systems are used.

Sample Assignment Schedule

An assignment schedule is a simple summary showing which invoices are included in a submission.

| Invoice # | Customer | Invoice Date | Invoice Amount |

|---|---|---|---|

| INV-10421 | ABC Manufacturing, Inc. | 03/01/2026 | $18,500.00 |

| INV-10422 | XYZ Logistics LLC | 03/02/2026 | $9,750.00 |

| INV-10423 | Brightline Staffing | 03/03/2026 | $12,300.00 |

| INV-10424 | Northshore Distributors | 03/04/2026 | $6,980.00 |

| INV-10425 | Summit Services Group | 03/05/2026 | $14,250.00 |

Want to avoid delays? Let a Funding Explorer match you with the right factor the first time.

Funding the Invoice: When Advances are Released

After you submit an invoice and it’s approved and, if needed, verified, the factoring company usually sends your advance the same day or the next business day.

At this stage, you get part of the invoice amount upfront. The rest is held as a reserve and settled after your customer pays.

How Customers Pay: Lockboxes and Payment Flow

In most factoring setups, your customers are required to send payments to a lockbox or bank account in your business’s name. This account is managed by the factoring company.

This system ensures payments are applied correctly, reduces misdirected payments, and allows settlements to happen efficiently.

Your customers keep paying as usual. The only difference is where payments are sent.

What Happens After the Customer Pays

When a customer payment comes in, it’s deposited into a cash reserve account. The advance and fees are deducted, and the rest is sent to your business, usually by wire or ACH on scheduled days, often in batches.

For a deeper explanation of how reserves work, see Factoring Reserves.

What Happens When Customers Pay Late, Short Pay, or Don’t Pay

Late payments, short payments, or non-payment usually don’t interrupt your daily factoring process. However, these collection issues can delay settlement of reserve balances, result in a chargeback or repayment obligation, depending on the terms of the factoring agreement, or trigger additional monitoring or follow-up.

These situations are closely tied to how reserves and settlements work and are covered in more detail in our article about factoring reserves.

Part 2: What Happens Occasionally

These steps usually happen only when something changes, your business grows, or there’s extra risk.

Verification

In invoice factoring, verification is the process of confirming that an invoice represents completed services or delivered products and that the customer is expected to pay it under the agreed terms.

Verification is often misunderstood in factoring. Invoices are not verified every single time.

Whether verification happens depends on risk, your history, and whether anything has changed.

Verification usually happens when:

- A new customer is factored for the first time.

- An invoice amount is significantly larger than normal.

- Documentation is missing or inconsistent.

- A customer has a history of disputes or slow payment.

- The factor hasn’t seen recent activity for that debtor.

Verification is less likely in these situations:

- The customer is well-known and pays reliably.

- Invoices follow a consistent pattern.

- Supporting documents are clean and complete.

- Prior invoices have been paid on time.

Debtor Approval and Debtor Credit Limits

Even after your business is approved, each of your customers must also be approved for factoring.

Debtor approval typically happens:

- Before the first invoice is funded.

- When a new customer is added.

- When invoice volume increases significantly.

- If a customer’s credit profile changes.

Often, approved customers have their own credit limits within your overall account limit.

Debtor Monitoring

Factoring companies continuously monitor: invoice aging, payment patterns, disputes, and customer credit health.

This monitoring is mostly passive and based on data. It doesn’t mean your invoices are always checked or that collections are aggressive.

When payments slow, disputes come up, or there’s news that raises questions about a customer’s finances, the factor may step in to review what’s going on.

Submitting Compliance Information

To control risk, some factoring companies regularly ask for updated documents and reports. These requests tend to happen early in your relationship or if your account is higher risk.

The information requested typically includes monthly bank statements, updated accounts receivable aging, and customer concentration reports.

Other factoring companies don’t request monthly paperwork but may have special requests if something changes, like increased volume, new owners, or shifts in payment behavior.

Mailing Notices of Assignment (NOA)

A Notice of Assignment (NOA) is a formal letter delivered to your customers to let them know that the factoring company has bought the invoices and to give them new payment instructions. This helps make sure payments go to the right place and reduces the risk of mistakes or delays.

These Notices of Assignment are typically sent:

- To all the debtors you plan to factor at the beginning of the relationship.

- Anytime a new debtor is added and factored.

- Occasionally, if payment instructions change.

Increasing Your Facility Line When Your Needs Grow

Factoring lines for your entire account and per debtor are reviewed from time to time. Factoring companies approve line increases typically when:

- The invoice volume grows consistently.

- Customers pay on time.

- There are no invoice disputes.

Sometimes you need to ask for those line increases, but many factors automatically do it when they see growth and the relationship is running smoothly.

Summary: Everyday vs. Occasional in Invoice Factoring

A quick way to see what typically happens each funding cycle vs. what usually only happens when something changes.

| Happens Every Funding Cycle | Happens Occasionally |

|---|---|

Issue invoices after work is completed or products are delivered. Submit invoices (portal, email, or hybrid) with the required documents. Receive an advance once the invoice is approved (and verified if needed). Customer pays to the lockbox or designated payment account. Fees are applied and the reserve balance is settled after collection. | Verification (more likely for new debtors, large invoices, missing docs, or recent disputes). Debtor approval and setting/changing debtor credit limits. Notices of Assignment (NOA) when starting or when new debtors are added (and if payment instructions change). Compliance requests (e.g., monthly bank statements, AR aging, concentration reports), often early on or when risk changes. Line increases when volume grows and the relationship is running smoothly (automatic or by request). |

How Funding Explorer Helps

Funding Explorer acts as an independent advisor, helping you understand how factoring really works and connecting you with factoring companies that fit the way your business operates day to day.

We focus on finding the right partners so your cash flow stays steady and the process stays easy as your business grows.

Analia Miguel is an MBA and former CPA with 20+ years in business finance and marketing, including 14 years in alternative business finance. She helps business owners understand their funding options and choose cash flow solutions that truly fit their needs.

Get Expert Guidance at No Cost

Cut through the noise and skip the confusion. Our experts, with over 20 years of experience in business finance, will match you with the factoring program that truly fits.