Quick Summary

Factoring isn’t meant to replace bank financing. It’s designed to work alongside it. This article explains how businesses use factoring strategically within a funding stack to support growth, manage timing gaps, and improve cash flow, even when cheaper bank capital is available.

Many businesses think factoring only makes sense if they can’t get bank financing. In reality, factoring often works best alongside traditional bank financing, not as a replacement for it.

The real question isn’t just if factoring is cheaper than a bank loan. It’s whether your current mix of financing matches how your business grows, bills customers, and gets paid.

This article explains how factoring fits into a modern funding stack, how it works with existing debt, and why using factoring effectively can make sense even if cheaper capital is available.

The Mistake Most Businesses Make When Comparing Financing

Most people compare financing options based only on the interest rate.

- Bank line of credit: low interest

- Factoring: higher cost

At first glance, the choice seems obvious. But financing decisions rarely go wrong because the rate was too high. They usually fail because the structure didn’t fit how cash actually moves through the business.

- Banks are designed to fund predictable, stable operations.

- Factoring is designed to fund variable, invoice-driven cash flow.

When those roles aren’t clear, businesses may not fund growth enough or end up paying too much for emergency capital later.

What “Your Funding Stack” Really Means

A funding stack is the mix of financing tools a business uses together, not just the cheapest option.

A typical stack might look like this:

- Bank line of credit for base operating capital

- Equipment loans for long-term assets

- Factoring for receivables tied to growth or timing gaps

- Short-term high-cost debt is only used if the main structure doesn’t work.

Each layer serves a different purpose.

Problems come up when one part of the stack is used for something it wasn’t meant to handle.

The Constraint Problem Behind “Cheap” Capital

| Financing Type | Relative Cost | Structural Flexibility |

|---|---|---|

| Bank Line of Credit | Low | Highly constrained |

| Equipment Loan | Low | Very restrictive |

| Invoice Factoring | Medium | Flexible and adaptive |

| Short-Term / Emergency Debt | Very high | Extremely restrictive |

Bank financing costs less because it comes with more restrictions. Factoring is more expensive because it offers more flexibility. The goal isn’t to avoid higher-cost capital completely, but to use it only when its flexibility is worth the extra cost.

Why Cheap Bank Money Can Still Create Cash Flow Problems

Bank lines of credit are capped by borrowing bases, covenants, and re-underwriting timelines.

These restrictions can strongly affect access to capital to support growth.

Here’s a simple example:

- Your company’s monthly cash flow needs: $300,000

- Your bank line available: $200,000

- Amount in outstanding receivables: $400,000

- There’s a growth opportunity that requires another $100,000 in working capital.

The bank line is cheaper, but it can’t cover all your working capital needs.

At this point, your business has three choices:

- Option One: Grow slowly.

- Option Two: Take on a very expensive, short-term emergency debt (such as online loans or MCAs).

- Option Three: Use factoring selectively

Let’s see how we can use factoring services to cover this cash flow gap.

How to Use Factoring to Complement Bank Financing

This company has a bank line that comfortably covers its basic cash flow needs but is experiencing growth that is creating a temporary working capital gap.

Here are our simple assumptions for this example.

- The total amount of working capital needed is $300,000.

- The bank line available: $200,000 at 9% APR interest-only

- The company still needs to fund an additional $100,000

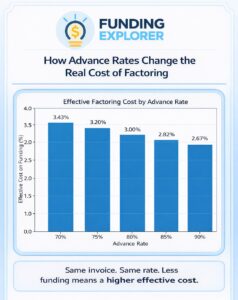

- The company needs to factor only enough invoices to generate $100,000 in extra cash flow.

- The factoring company agreed to a factoring advance of 85%

- The agreed factoring rate is 2.40% (for simplicity, the fee is applied to the invoice value)

- This company’s customers pay on average in 30 days.

First, let’s define how much invoice volume must be factored to get $100,000.

Considering the agreed advance rate is 85%, then the invoice volume that needs to be factored is = $100,000 ÷ 0.85 = $117,647.

Now, let’s estimate the factoring cost for that month by applying the factoring rate on the invoice amount: 2.40% × $117,647 = $2,823.53.

Next, let’s calculate the cost of bank financing that month.

For the $200,000 borrowed, the interest paid would be $200,000 × (9% ÷ 12) = $200,000 × 0.0075 = $1,500.

Next, let’s calculate the total financing cost for that month.

- Total financing cost (factoring plus bank financing) = $2,823.53 + $1,500 = $4,323.53.

Finally, let’s get the effective blended cost on the total $300,000 working capital.

- Effective rate = $4,323.53 ÷ $300,000 = 1.44% per month.

Yes, factoring is more expensive than bank financing. But when it’s used only to fund incremental growth needs, the blended cost is often reasonable.

In many cases, it’s far less costly than emergency capital or passing on growth opportunities.

When Factoring Makes Sense Even With a Bank Line

When it’s set up correctly, factoring doesn’t replace bank financing. It fills in the gaps that banks aren’t designed to cover.

Banks are great at funding predictable, stable needs. Factoring works great when cash flow is tied to timing, growth, or variability. Used together, they can actually make your financing more efficient, not more expensive.

The following uses often justify the use of factoring together with a bank line:

- Fund operations to support new or fast-growing customers.

- Meet seasonal or uneven cash flow needs.

- Get a cash flow infusion during a rapid scale-up.

- Avoid breaching covenants or over-advancing a bank line.

In many cases, factoring protects your bank relationship instead of competing with it. It gives you flexibility without forcing the bank to stretch beyond its comfort zone.

Common Friction Points (and How They’re Usually Solved)

Using factoring alongside a bank line does require some coordination, but these situations are common and usually manageable.

Bank liens on receivables

Banks almost always want first claim on accounts receivable. Factoring, by nature, requires those receivables to be assigned to the factor. That sounds like a conflict, but it’s usually not.

What to do about this:

Through subordination agreements or portfolio splits, where each lender clearly funds a different portion of receivables. Once that’s defined, both facilities can operate without interfering with each other.

Covenant pressure during growth

Rapid growth is great until it starts pushing up against leverage or liquidity covenants tied to your bank financing.

How to solve this situation:

Factoring can provide you with extra cash tied directly to your receivables without adding more traditional debt. In many cases, this flexibility actually helps relieve covenant pressure rather than increasing it.

The takeaway is simple: these aren’t deal-breakers. They’re structural questions. When properly addressed, factoring and bank financing can work together smoothly, each doing the job for which it’s best suited.

A Simple Allocation Rule That Actually Works

Instead of asking yourself, “Should I use factoring?”, try asking:

Which funds should be covered by which financing tool?

| Funding Need or Use Case | Best-Fit Financing Tool |

|---|---|

| Fixed operating expenses | Bank line of credit |

| Stable, predictable receivables | Bank line of credit |

| Growth-driven sales | Factoring |

| New customers or contracts | Factoring |

| Seasonal revenue spikes | Factoring |

| Equipment purchases | Equipment financing |

Here’s a simple rule of thumb:

- Use bank loans for steady, predictable needs.

- Use factoring when your cash flow is more variable.

Short Real-World Scenarios

These situations come up all the time. They’re good examples of how factoring is actually used in practice, not as a replacement for a bank, but as a complement when timing or growth creates pressure.

Scenario 1: The Bank Line Couldn’t Grow Fast Enough

A distributor had a bank line that worked well for day-to-day operations. The problem wasn’t access to credit; it was speed. New contracts came in faster than the bank could increase the line.

Instead of slowing growth or taking on expensive short-term debt, the company layered in factoring only for invoices tied to the new business.

What happened:

Growth continued, cash flow remained stable, and the bank relationship remained intact, with no covenant issues or emergency financing.

Scenario 2: Factoring as a Temporary Bridge

A services company knew its bank line would likely be expanded, but the re-underwriting process would take several months.

Rather than wait or strain cash flow, the company used factoring as a temporary solution during that gap.

What happened:

Yes, factoring costs more than a bank line. But since it was only used for a short time, the total cost stayed reasonable, and the business didn’t miss out on growth while waiting for the bank.

Scenario 3: Replacing Emergency Debt, Not the Bank

Another company already had a bank line, but timing gaps forced it to take on a single MCA to keep things moving.

Factoring was introduced, and part of the early funding was used to pay off the MCA. The bank line remained the primary source of capital.

What happened:

Daily payment pressure disappeared, cash flow stabilized, and the overall funding mix became both cheaper and more predictable.

The Real Decision Isn’t Cost, It’s Fit

Factoring isn’t just for emergencies. It’s a useful tool.

If you use it the wrong way, it can be costly.

If you use it wisely, it’s efficient.

The businesses that get the most out of factoring are the ones that know why they’re using it, not just what it costs.

How Funding Explorer Helps Structure the Right Stack

At Funding Explorer, we help businesses focus on funding strategy instead of just picking individual products.

We help you:

- Evaluate how bank financing and factoring interact.

- Avoid accumulating unnecessary short-term debt.

- Set up factoring so it works well with your bank financing, not against it.

The goal isn’t just to get more financing. It’s to find the right mix for your business.

Analia Miguel is an MBA and former CPA with 20+ years in business finance and marketing, including 14 years in alternative business finance. She helps business owners understand their funding options and choose cash flow solutions that truly fit their needs.

Last Updated: February 27th, 2026

Business Funding Expert Insights

We Help You Find The Right Factor

Every factoring company prices and structures deals differently. Funding Explorer matches you with partners that fit your cash flow and financing stack.