What a Factoring Application Really Requires (and Why)

Learn what information factoring applications ask for, what really matters, and how to avoid delays or denials.

When business owners hear “factoring application,” they often expect a long, complicated process similar to a bank loan.

In reality, factoring applications are usually much simpler and much faster. Most take less than 10 minutes to complete.

The purpose of a factoring application isn’t to judge your personal credit or analyze years of financial statements. It’s to help the factoring company understand your receivables, your customers, and how invoices move through your business so they can assess payment risk.

This guide walks through what factoring companies actually evaluate during the application process, why each item matters, and how different answers affect approval, structure, or pricing before you apply.

What This Article Covers

To make it easy to navigate, here’s what you’ll find below:

- Why factoring applications are different from loan applications

- Do all factoring companies use the same application?

- The core information most factoring applications require

- Typical supporting documents requested

- Real-world examples of fixable application issues

- What can disqualify an application vs. what shapes the deal

- How long the application and approval process usually takes

- How Funding Explorer helps you apply the right way

To make this more concrete, we’ve also included real-world scenarios showing how common application concerns are evaluated in practice, including situations where approval was possible with the right structure.

Why Factoring Applications Are Different From Loan Applications

Factoring is not based primarily on your borrowing capacity or credit score.

Instead, factoring companies focus on one core question:

How confident are we that these invoices will be paid, in full and on time?

Everything in the application supports answering that question, directly or indirectly.

That’s why factoring applications are shorter than loan applications but still very specific about customers, invoicing, and payment behavior.

Do All Factoring Companies Use the Same Application?

No, not all factoring companies use the same application, but they all ask for similar basic information. The only thing that changes is how that information is gathered and evaluated.

The most important thing is not the format of the application but the completeness and accuracy of the information. The better the information you provide when you first submit it, the faster the evaluation will be and the fewer additional requests you’ll get later.

Ready to explore your options or apply? We’ll love to help!

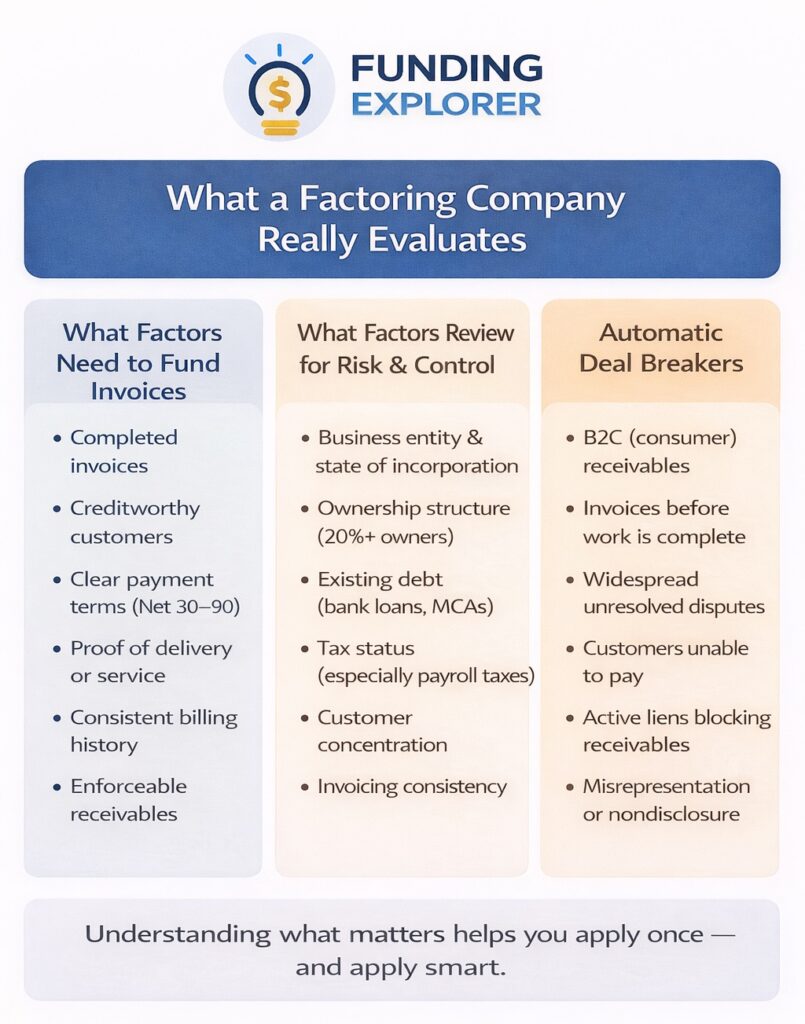

The Basic Information Most Factoring Applications Ask For

While every factoring company has its own application, most of them are trying to answer the same questions. That means they tend to ask for the same core information, even if it’s presented a little differently.

Here’s what you’ll almost always see and why it matters.

1. Information About Your Business

This is the foundation of the application. It’s mostly straightforward, and it’s not meant to be time-consuming or complicated.

You’ll usually be asked for things like:

- Legal business name and DBA if applicable

- Your company’s entity type (LLC, corporation, etc.)

- The state where your company was incorporated and the date of incorporation

- Your business address, phone, email, and other contact details

Why factoring companies need to know this:

This information confirms that your business legally exists, identifies the state laws that apply, and allows the factor to properly secure its interest in your receivables.

Is this an instant disqualifier?

Almost never. This information is largely administrative unless there are unresolved legal or compliance issues tied to the business.

2. Customer Information (Typically More Important Than Your Own)

This is where factoring applications really differ from loan applications.

Factoring companies care deeply about your customers because your customers, not you, are the ones paying the invoices.

Most applications ask for:

- Your customer names and addresses (often just your top 5–10)

- The estimated monthly billing per customer

- Payment delays usually aren’t uncovered here. Those tend to show up later when the factor reviews your accounts receivable aging.

Why this information matters:

Customer credit quality and payment behavior drive approval, advance rates, and pricing far more than your company’s size or age.

Instant disqualifier?

Yes, if the invoices are consumer (B2C) instead of business-to-business or government (B2B/B2G), or if customers clearly lack the ability or willingness to pay, your application will be rejected.

3. Invoicing and Payment Terms

Next, the underwriter wants to understand how and when invoices are created.

Most applications ask:

- If pre-billing exists (billing before product or service delivery)

- What are your standard payment terms

Why this section matters:

Factoring companies only buy invoices for completed work and enforceable payment obligations. Invoices tied to future performance, milestones, or retainage often require special structuring.

Instant disqualifier?

Yes, if invoices are issued before work is completed and can’t be enforced, factoring usually isn’t available in its standard form.

4. Ownership Information (and Why Factors Ask for It)

This section often causes confusion, so it’s worth addressing directly.

Most factoring applications ask for:

- Owner names

- Ownership percentages

- Disclosure of any owner with 20% or more ownership

They’ll also often ask whether those owners:

- Are current on personal tax obligations

- Have had recent bankruptcies or judgments

Why this ownership information matters:

Factoring isn’t based on personal credit, but factors still look at control, transparency, and character risk. Owners with meaningful ownership influence billing practices, disclosures, and how disputes are handled.

Here’s an important clarification:

Past financial challenges do not automatically disqualify your application. As long as you honestly disclose them and explain whether issues have been resolved, you may still get approved.

Can ownership issues be an instant disqualifier?

Rarely, except in situations involving the following:

- Undisclosed bankruptcies

- Unresolved tax liens that interfere with receivables

- Active legal restrictions that block assignment

5. Financial Information: What’s Required (and What Isn’t)

Because factoring is not underwritten like a bank loan, instead of full financial statements, most applications ask for a high-level overview, such as:

- Estimated monthly revenue

- Existing financing (bank loans, MCAs, online lenders, etc.)

Margins are rarely asked directly because factors are generally known industry standards. They may ask questions only if something appears far outside expectations.

Why this basic financial information matters:

This information gives the underwriter context, how large the operation is, what obligations already exist, and the general financial situation of your business.

Important note:

Excessive MCA or short-term debt can be disqualifying. Bank loans often require subordination so the factor can be in the first position. In some cases, proceeds from early factoring funding can be used to pay off controllable short-term debt.

Instant disqualifier?

Rarely, except when short-term debt overwhelms cash flow or prevents full control of receivables.

Supporting Documents You’ll Usually Be Asked For Next

Together with the basic information, factoring companies typically request documents to verify what was provided.

This is the typical support documentation requested:

- A few sample invoices

- An accounts receivable aging report

- An aging report for accounts payable

- Customer contracts or purchase orders, if applicable to your operations

Proof of delivery or completion is usually required when invoices are submitted for funding, not during the application itself.

Some factors may request financial statements for higher-risk deals or specialized structures, but this isn’t universal.

Simplify the entire application process. Get expert help in minutes.

Real-World Examples of Application Issues That Can Be Fixed

To clarify special situations, here are a few real-world scenarios that come up often.

Scenario 1: A Single MCA That Was Snowballing

Situation

A logistics company had strong customers and consistent invoicing, but it was carrying one MCA with daily payments. As cash tightened, the MCA balance became harder to manage and started compounding the pressure.

The owner assumed factoring would be declined.

What actually happened

The factor approved the business based on customer quality and invoice consistency. Instead of requiring the MCA to be paid off upfront, a portion of the proceeds from the first four invoice submissions was used to cancel the MCA debt.

This was the final outcome:

Within the first month, the MCA was fully paid off. Daily payment pressure disappeared, cash flow stabilized, and the business was able to focus on growth.

Key takeaway

A single MCA is often a cash-flow problem, not a deal breaker, especially when it’s disclosed and addressed upfront.

Scenario 2: A Bank Loan That Needed Coordination, Not Elimination

Situation

A manufacturing company had an existing bank line of credit and assumed that meant factoring wasn’t possible.

What actually happened

The factor required a subordination agreement, so the factor had the first position in collecting the receivables. Once coordinated with the bank, the deal moved forward.

Outcome

The company kept its bank relationship, added factoring to support growth, and avoided stacking expensive short-term debt.

Why this matters

Bank debt doesn’t block factoring. It just needs to be structured correctly.

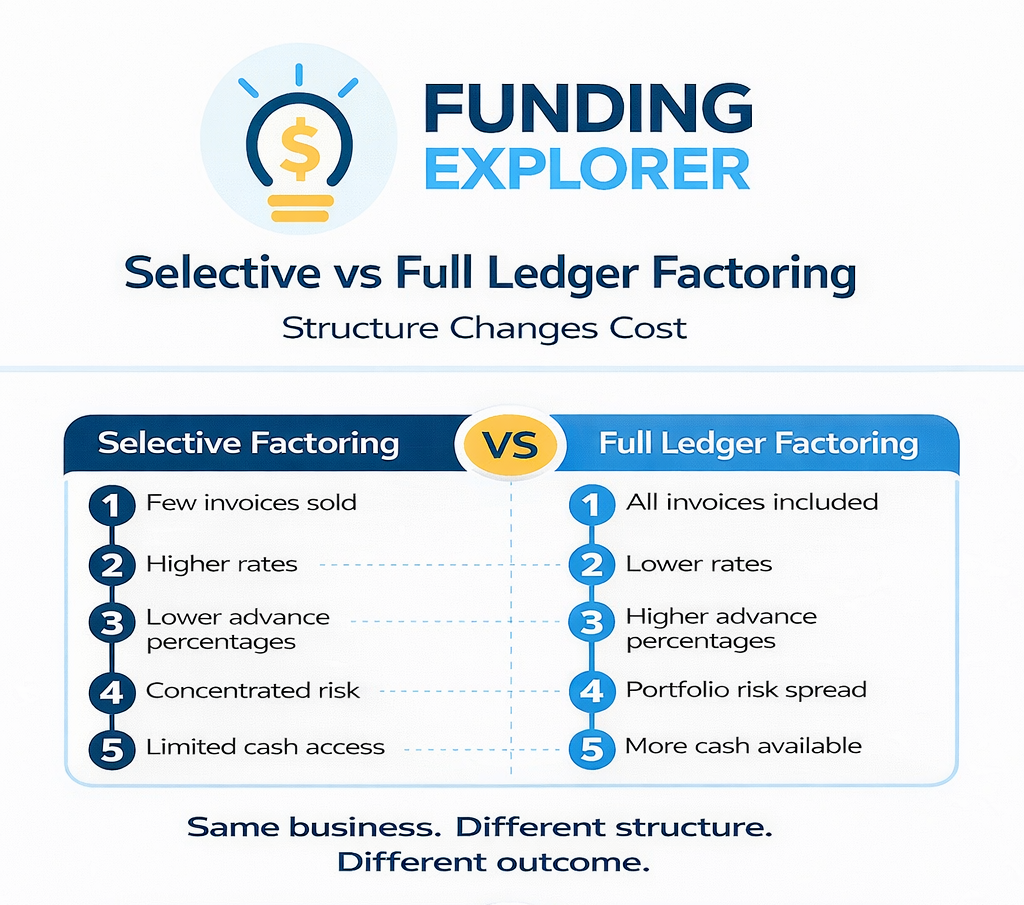

Scenario 3: Customer Concentration That Changed the Structure, Not the Outcome

Situation

One customer accounted for 65% of the company’s revenue, and the owner assumed this would prevent approval.

What actually happened

The factor adjusted the advance rates and reserves to reflect concentration risk instead of declining the deal.

Outcome

The company did qualify for factoring, but the terms were adjusted to match the portfolio risk.

Want to avoid delays? Let a Funding Explorer match you with the right factor the first time.

What Can Disqualify an Application vs. What Shapes the Deal

While many application items are informational, a small number of issues can stop an application outright. Most others affect structure and pricing, not eligibility.

Below is how factors typically think about this.

Clear Disqualifiers (Non-Negotiable)

| Issue | Impact |

|---|---|

| B2C receivables | Disqualifying. Factoring requires B2B or B2G invoices. |

| Invoices issued before work is completed | Disqualifying. Factoring requires products or services delivered. |

| Invoices tied to future milestones or retainage | Disqualifying unless specially structured. |

| Customers unable or unwilling to pay | Disqualifying. No payment source means no factoring. |

| Widespread unresolved disputes | Disqualifying until resolved. |

| Misrepresentation or nondisclosure | Disqualifying. Transparency is mandatory. |

| Legal restrictions on receivable assignment | Disqualifying unless removed. |

Fixable or Structure-Dependent Issues (Context Matters)

| Issue | How It’s Typically Handled |

|---|---|

| Bank loan with lien on receivables | Subordination so the factor is in first position. |

| MCA or short-term high-cost debt | Often paid down using proceeds from early invoice funding. |

| Past bankruptcy (fully disclosed) | Commonly workable if resolved and transparent. |

| Tax debt (non-employment, being addressed) | Depends on lien status and repayment plan. |

| Customer concentration | May affect advance rates or require exclusions. |

| Industry-driven dilution | Handled through reserves and documentation requirements. |

| Seasonal or uneven revenue | Requires a structure aligned with cash-flow timing. |

| Low margins | May affect usefulness and structure more than eligibility. |

High-Risk Flags (Require Deeper Review)

| Issue | Why It Matters |

|---|---|

| Payroll or employment tax liens | Can attach to receivables and block funding. |

| Recent undisclosed bankruptcy | Raises transparency and trust concerns. |

| Heavy daily or weekly payment obligations | Can disrupt cash flow and collections. |

| Inconsistent invoicing or weak documentation | Increases disputes and dilution risk. |

| Customers paying far beyond stated terms | Impacts predictability and reserve timing. |

Get answers fast, avoid mistakes, and move forward with confidence.

How Long Does a Factoring Application Take?

For most businesses:

- Application: under 10 minutes

- Document review & approval: often same business day

How Funding Explorer Helps You Apply

At Funding Explorer, we help businesses apply once, not repeatedly.

We work with multiple factoring partners and:

- Assess real-world eligibility before you apply.

- Flag potential issues early.

- Match you with factors that accept your specific situation.

- Help structure deals that accommodate special cases.

There’s no cost to you.

The result is less wasted time, fewer declines, and a higher chance of approval on the first attempt.

If you want the fastest approval with the right factor, we’re here to help.

Analia Miguel is an MBA and former CPA with 20+ years in business finance and marketing, including 14 years in alternative business finance. She helps business owners understand their funding options and choose cash flow solutions that truly fit their needs.

Last Updated: February 24th, 2025

Invoice Factoring Expert Insights

Apply Once. Save Time & Avoid Hassle

Applying through Funding Explorer means one application, smarter matching, and fewer declines. We connect you with factoring partners that fit your business and situation, at no cost to you.