Quick Summary

A disputed invoice under factoring can sometimes affect more than just one payment. Factors look at the entire portfolio, especially customer concentration and funded exposure. This article explains how disputes are evaluated and what businesses can do to protect cash flow and avoid unnecessary funding interruptions.

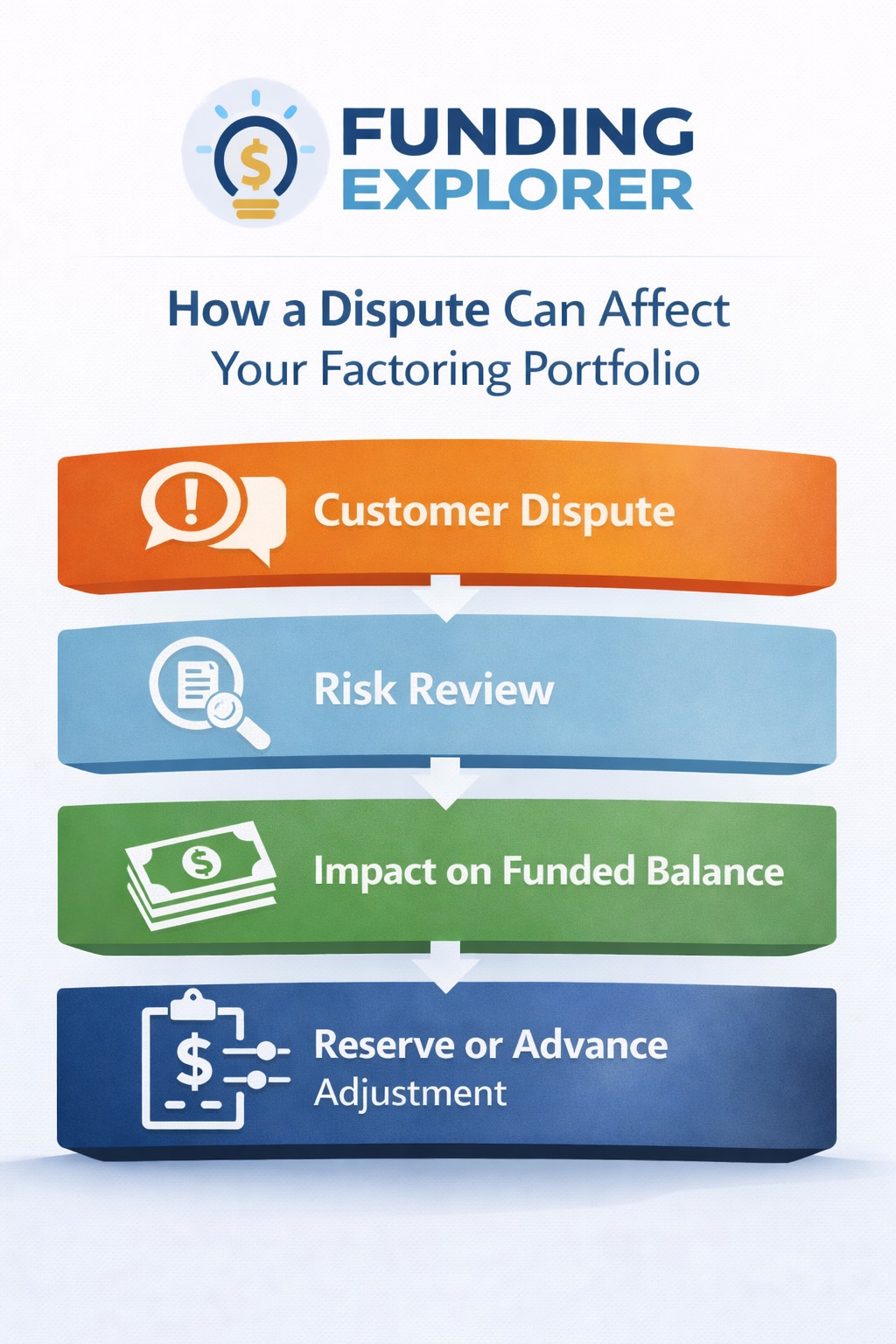

Invoice disputes happen, even in well-run businesses with solid customers. What surprises many companies is how big a dispute can feel once factoring is involved.

Something that used to be a routine customer issue can suddenly affect funding, reserves, or availability. That’s because factoring doesn’t look at invoices one at a time. It looks at your entire receivables portfolio, with special attention to who your customers are, how concentrated your sales are, and how invoices actually get paid.

Once you understand that, the way factors react to disputes makes much more sense.

What Is an Invoice Dispute in Factoring?

Factoring Companies Look at Your Receivables as One Portfolio

Under factoring, invoices aren’t treated as standalone transactions. All eligible invoices across all customers are grouped together and used as shared collateral for the funding line.

Advance rates, reserves, and availability are calculated against total exposure, not individual invoices.

When uncertainty shows up in one part of the portfolio, risk is adjusted across the portfolio, not just on the disputed invoice. That structure is the core reason disputes can feel bigger under factoring.

Why Disputes Are Really About the Customer, Not the Invoice

In factoring, the real credit risk isn’t the invoice. The credit risk is based on the customer who is expected to pay it.

Factoring companies evaluate disputes primarily at the debtor level because payment behavior tends to repeat.

They monitor things like:

- Payment consistency

- Dispute frequency

- Short-pay or offset behavior

- Documentation issues

A dispute from a customer that represents 5% of your receivables is treated very differently from a dispute involving a customer that represents 40%.

In most cases, the concern isn’t the disputed invoice itself. The concern is what that dispute might signal about other invoices already funded or future invoices tied to the same customer.

Why Disputes on Factored Invoices Are Treated More Seriously

Disputes matter most when they involve invoices that have already been factored and funded.

In those cases, the factor has already advanced cash and is exposed to the risk of not being repaid.

A dispute over a factored invoice can raise concerns that other factored invoices from the same customer may also be delayed, short-paid, or challenged.

The larger the total amount already factored for that customer, the more quickly the factor may adjust advances or reserves to protect that exposure.

Example: How Concentration Can Affect Funding During Customer Disputes

A staffing company had one large customer representing 35% of receivables.

When two funded invoices were disputed over documentation timing, the factor paused new advances from that debtor until clarification was received.

Funding resumed once documentation was corrected, but the temporary adjustment highlighted the risk of concentration.

Exposure Comparison Table (Small vs Large Debtor)

| Scenario | Portfolio Impact | Likely Factor Response |

|---|---|---|

| 5% Customer, Small Invoice | Limited | Isolated review |

| 40% Customer, Large Funded Balance | Significant | Funding adjustments likely |

How Invoice Size Changes the Impact

Invoice size also matters more than many businesses expect.

A portfolio made up of many smaller invoices spreads risk naturally. A portfolio dominated by fewer, larger invoices concentrates risk.

One large, delayed invoice can affect availability much more than several smaller ones, even if total monthly revenue remains the same.

That’s why factors pay close attention to both customer concentration and invoice size.

When Disputes Start Affecting Advances and Reserves

When disputes are material or start repeating, factors may adjust risk across the portfolio. That can include:

- Pausing funding on new invoices from the affected customer

- Increasing reserve buffers

- Tightening eligibility standards

- Slowing funding while issues are reviewed

These actions aren’t penalties. They are portfolio-level risk adjustments meant to protect the funding structure until uncertainty is resolved.

When Issues Appear Across Multiple Customers

One dispute with one customer is usually manageable. But when disputes or payment delays start appearing with several customers, the analysis changes.

At that point, factors are less focused on individual debtor credit and more focused on whether there is a broader operational issue.

Common concerns include billing inconsistencies, documentation gaps, or process strain caused by growth.

When disputes are widespread, the risk assessment shifts from customer behavior to client operations.

Who Resolves Disputes Under Factoring

Even with a factor involved, the business is responsible for resolving disputes.

The factor manages exposure and funding decisions but relies on the client to address customer issues directly.

Clear communication matters because uncertainty is treated as risk. From a factor’s perspective, knowing there is a problem is usually better than not knowing what’s happening.

Tips to Keep Disputes From Snowballing

When disputes start appearing, these actions matter most:

- Treat disputes involving large or highly concentrated customers as urgent, because they carry outsized risk for the entire portfolio.

- Communicate early and start working on the issue before it becomes a bigger problem.

- Make it clear whether a dispute is a one-time issue or something that keeps happening.

- If disputes start showing up across several customers, take time to identify internal process problems that may be causing them and work to resolve the issues.

Handled quickly and transparently, many disputes stay contained instead of becoming portfolio-level problems.

How Funding Explorer Supports Factoring Clients

In factoring, the real concern isn’t the dispute alone, but what it shows about concentration and risk in the portfolio.

At Funding Explorer, we help clients understand how disputes are viewed by factors and how to manage them so funding stays predictable when issues arise.

FAQ About Invoice Disputes in Factoring Relationships

Can just one disputed invoice affect funding for other invoices?

Yes, it can. Because factoring looks at all receivables together, a dispute tied to a large customer or a large unpaid balance can lead to temporary funding changes until the issue is understood and resolved.

Why does customer concentration matter so much when an invoice dispute happens?

When one customer represents a large share of receivables, a dispute becomes a portfolio risk issue rather than an isolated invoice problem.

What if invoice disputes start happening with several customers?

When problems show up with many customers, the factor may think something inside the business isn’t working right and may slow things down until it’s fixed.

Who is responsible for resolving customer disputes under factoring?

The business fixes the problem with the customer, and the factor decides how funding is handled while the issue is being resolved.

Analia Miguel is an MBA and former CPA with 20+ years in business finance and marketing, including 14 years in alternative business finance. She helps business owners understand their funding options and choose cash flow solutions that truly fit their needs.

Last Updated: March 13th, 2026

Business Funding Expert Insights

Need help evaluating your factoring options?

Funding Explorer works with multiple factoring companies and helps you find the right fit for your portfolio, at no cost to your business. We guide you through structure, risk considerations, and lender selection so your funding remains predictable.